Contents

Kevin Carmichael: It feels like Canada is entering a new phase of persistently strong demand for workers

Article content

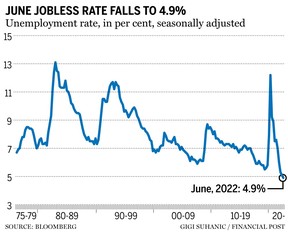

Canada’s red-hot labour market cooled a little in June. It’s now only historically hot. Here’s what you need to know:

Advertisement 2

Article content

New paradigm

Once the big brains at the Bank of Canada and elsewhere get the current inflationary episode figured out, they probably will spend some time thinking about a new working definition of full employment.

Ahead of the Great Recession a decade ago, a number of around six per cent was thought to be about as low as Canada’s jobless rate could go before that much hiring started to create more demand than the economy could handle, and thus stoked inflation.

With that in mind, consider the unemployment rate in June: 4.9 per cent, compared with 5.1 per cent in May.

The rate has now been below six per cent since the end of 2021, and had effectively settled at around 5.5 per cent ahead of the COVID crisis. To be sure, given that inflation is testing eight per cent, it’s safe to assume that economists will conclude that 4.9 per cent is more than Canada’s relatively unproductive suppliers of goods and services can handle. But it does feel like Canada has entered a new phase, as technological disruption and a shrinking number of older workers combine to create persistently strong demand for workers.

Advertisement 3

Article content

Wages

Employment actually dropped by about 43,000 positions in June, Statistics Canada said. (The jobless rate, which measures the number of people who say they are actively seeking employment but can’t find a job, dropped because fewer people were looking for jobs.)

That’s normally the headline number. But the most important indicator in Statistics Canada’s monthly Labour Force Survey these days is wage growth. That’s because the central bank is watching wages closely to make an educated guess about whether inflationary pressures that have been concentrated in prices for goods are spreading. If wages accelerate too fast, the Bank of Canada will see that as evidence that expectations of entrenched inflation are taking root, raising the odds of a self-fulfilling spiral. Central bankers have only one way to break such a psychology: higher interest rates.

Advertisement 4

Article content

-

Soaring inflation expectations raise odds of super-sized Bank of Canada hike

-

Canada to fall into ‘moderate and short-lived’ recession next year, RBC warns

-

Canada’s trade surplus just blew away expectations

Average hourly wages surged 5.2 per cent from June 2021, compared with a year-over-year increase of 3.9 per cent in May. That’s slower than inflation, but high by recent historical standards: the average annual gain between February 2010 and February 2020 was 2.4 per cent.

Inflation has exceeded three per cent for more than a year, so workers’ wage expectations almost certainly have been rising along with the cost of living. And they are in a good position to bargain, thanks to record job vacancies. Statistics Canada also observed that there were about 250,000 fewer self-employed workers in June than at the start of the pandemic, in part because the relative ease of securing a good job makes the risk associated with self employment less appealing. Some five per cent of those who worked for themselves in May became employees in June, more than twice as high as the average between 2016 to 2019, the agency said.

Advertisement 5

Article content

Individuals getting the raises probably are happy, but Bank of Canada Tiff Macklem likely will be fretting about that number as he considers what to do with interest rates ahead of his next policy announcement on July 13.

Recovery like no other

Macklem (and other central bankers) are absorbing considerable criticism for letting inflation get out of hand, and the leader of Canada’s central bank concedes that he misread the signals being sent by bubbling price pressures more than a year ago. In hindsight, the response to the COVID recession was probably excessive. That’s why most central banks have accelerated their efforts to get interest rates back to more normal levels.

However, today’s threat (runaway inflation) makes it easy to forget what policymakers were attempting to do in the spring of 2020: orchestrate a recovery in record time in order to avoid the sort of social pain that came with the frustratingly slow recovery that followed the Great Recession.

Advertisement 6

Article content

One of the better indicators of scarring from an economic downturn is long-term unemployment. The longer people are left on the sidelines of the economy, the harder it is to get back in, as skills erode and employers tend to favour candidates with recent experience. The long-term unemployed face having to settle for jobs beneath their capabilities, or marginalized, given the extent to which work is associated with status and happiness.

Last month, the number of people who had been without work for 27 continuous weeks dropped about 11 per cent, to 185,000. Statistics Canada said the drop was entirely explained by some 22,000 people who had been unemployed for a year or more finding jobs.

The long-term unemployed represented about 0.9 per cent of the labour force in June, the same as in February 2020. Statistics Canada said that was a faster drop than in previous recessions. For example, long-term unemployment didn’t return to pre-recession levels after the 2008-2009 financial crisis until May 2019.

Advertisement 7

Article content

In other words, it took the labour market a decade to fully heal from Great Recession. Full recovery from the COVID recession took 28 months. Macklem didn’t get everything wrong.

Bottom line

The post-pandemic hiring boom probably has peaked. The drop in employment offset May’s gains and was the first decline unassociated with COVID restrictions since the start of the pandemic. Also, it’s hard to imagine the jobless rate can go much lower. Our desire to spend is bumping up against our ability to supply goods and services. Since there’s no easy way to ramp up supply of labour — or boost productivity — in the short term, the Bank of Canada will feel it has little choice but to curb demand, even if that means triggering a recession.

Advertisement 8

Article content

“With inflation pressures remaining elevated and the economy growing, the Bank of Canada remains highly likely to raise rates by 75 basis points next week,” Karl Schamotta, chief market strategist at Cambridge Mercantile Corp., advised his clients in a note. “Today’s numbers are reflective of a jobs market operating well beyond full employment, not one that is exhibiting recessionary tendencies.”

• Email: kcarmichael@postmedia.com | Twitter: carmichaelkevin

Listen to Down to Business for in-depth discussions and insights into the latest in Canadian business, available wherever you get your podcasts. Check out the latest episode below: